Beige Book Shocker: "Semiconductor Orders From China Plunged The Most Since The Collapse Of Lehman"

While the latest Beige Book released earlier today carried the usual boring mix of self-serving observations by Fed officials ("slight to moderate" growth in a quarter in which the Atlanta Fed sees GDP plunging to 0.5%) and a handful of enlightening anecdotes, all of which confirmed that the US economy was rapidly slowing as expected with the word "strong" appearing 37 times, compared to 58x in the January and 83x in October while the word "weak-" rose to 34x, up from 13x seven weeks ago and 19x in October, there was one stunner contained in today's release which may spell serious pain for stocks.

But first we bring your attention to chip and semiconductor bellwether Micron which tumbled as much as 6.2%, its biggest decline in a month, as Wall Street grows increasingly bearish on memory-chip pricing. According to analysis by DRAMeXchange, PC DRAM contract prices will be down a whopping 30% in the first quarter, and since inventory levels are still high, there is little hope of a reversal anytime soon. The Q1 price drop would be the worst since 2011, while a shortage of low-end CPUs is exacerbating the problem, eliminating an avenue for demand growth. "The overall market has thus entered freefall, meaning that large reductions in prices aren't going to be effective in driving sales," according to DRAMeXchange.

As a result, Cleveland Research cut its 2019 revenue estimate to $24 billion from $25.5 billion, citing those same DRAM price headwinds.

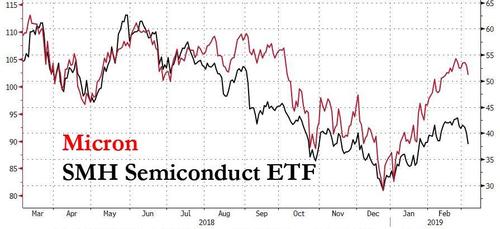

And, as shown below, even though Micron tumbled in the past week after surging nearly 50% from its December lows, retracing nearly half of the gain, the broader semiconductor space - as represented by the SMH VanEck Semiconductor ETF - has yet to follow in Micron's footsteps; in fact it appears to be immune from the renewed concerns surrounding the global economy and the US-China trade negotiations in particular.

Which brings us back to today's beige book, and one specific disclosure which suggests that the broader semiconductor space - by many seen as a leading indicator for China's economy - is about to implode.

As the Boston Fed section of the Beige Book noted, there were two key references to the semiconductor industry. The first one, while not critical was more of an amusing anecdote why the US labor market has been persistently "strong" as most high frequency indicators have been rolling over. This is what the Beige Book said about the labor market in the context of the semi sector:

A semiconductor manufacturer facing big declines in demand from China put a hiring freeze in place, but they were reluctant to institute layoffs since it takes three to six months to train new workers.

It was the second Boston Fed reference to the semi sector that was far more critical: this is what the Boston Fed said regarding anecdotal reference to manufacturing and related services.

Two [firms] reported substantial drops in sales and two reported significant weakness. The two firms that reported serious issues were a semiconductor manufacturer and a furniture builder.... The semiconductor firm sells mostly to the auto industry and said that a 40 percent drop in new orders from China was the biggest fall in sales since the collapse of Lehman in 2008. Two other firms, both with heavy exposure to semiconductors, said that the market had slowed significantly since earlier in 2018 - Link.

So let's see: Micron is tumbling, and is down over 30% from where it was a year ago as DRAM pricing plummets confirming demand has imploded, even as the broader semiconductor ETF is basically where it was a year ago this time. And yet, according to the most real-time, and some would say honest representation of the industry (as anonymous Beige Book respondents don't have to worry about their shareholders dumping their stock so they tend to be far more honest than more publicly reporting companies), a semi firm just reported a "40 percent drop in new orders from China" which was "the biggest fall in sales since the collapse of Lehman in 2008."

As for what this observation means for China's economy, for which the semiconductor space has long been seen as the best proxy, we leave it up to readers to make up their minds just how bullish this news is and whether it merits the S&P trading just a few percent below its September all time highs.

No comments:

Post a Comment