DOMINOES (BANKS)FALLING HSBC To Slash 10,000 More Jobs As Ax Falls On "Project Oak"AND FROM THIS ARTICLE--Hong Kong Violence Sends Home Prices Tumbling Over 20%, Puts HSBC In The Crosshairs

HSBC To Slash 10,000 More Jobs As Ax Falls On "Project Oak"

Amid plunging European (and global) interest rates, Brexit uncertainty at home, and social unrest abroad (collapsing Hong Kong property prices and ATMs running out of cash), UK-based banking behemoth HSBC is reportedly implementing a global cost-cutting effort known internally as "Project Oak."

On top of around 4,700 planned layoffs, The FT reports that new interim CEO Noel Quinn - following the departure of John Flint - is planning cost-cutting measures that could result in 10,000 layoffs. According to one of the people briefed on the matter:

“We’ve known for years that we need to do something about our cost base, the largest component of which is people - now we are finally grasping the nettle."

“There’s some very hard modelling going on. We are asking why we have so many people in Europe when we’ve got double-digit returns in parts of Asia.”

HSBC’s latest cost-cutting drive will reportedly focus mainly on high-paid roles, and will be implemented under a scheme known as “Project Oak”, which tried to encourage executives and managers to shrink their teams by offering funding from a central pot of money to cover redundancy payouts.

HSBC's move comes as global banks (Deutsche Bank most recently following cuts at Barclays, SocGen, and Citi) make tens of thousands of staff redundant as the industry contends with low or negative interest rates and weak investment banking revenues.

Finally, The FT notes that HSBC could announce that it has begun the cost-cutting exercise when it reports third-quarter results later this month, one of the people said, although the bank has not yet made a final decision on when to make the plan public.

Hong Kong Violence Sends Home Prices Tumbling Over 20%, Puts HSBC In The Crosshairs

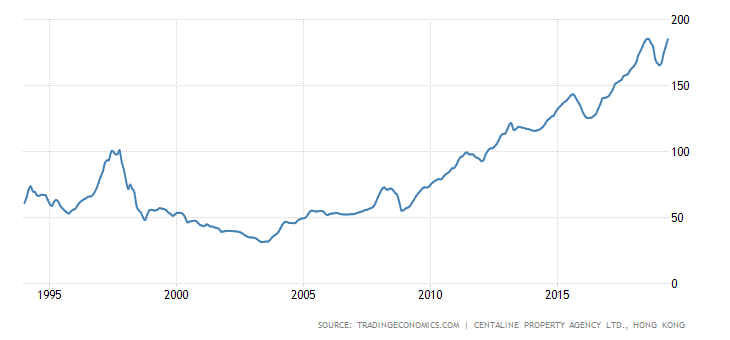

Oct. 1 might be remembered as an important turning point for the Hong Kong property market. In the wake of riots that saw an unprecedented escalation in violence (police shot a teenager with live fire for the first time), SCMP reports that the Hong Kong property market has seen prices reduced by as much as 20%.

But as protests threaten to drag on into a fifth month despite a police crackdown and a new attempt by the city's executive council to discourage protesters by banning masks - something that has, so far, only served to infuriate the protesters and encourage more violence - it's going to be difficult to call a bottom in the Hong Kong property market, formerly one of the most unaffordable markets in the world, as many Hong Kongers flee to places like Taiwan and Malaysia.

Many also think just holding cash right now might be the safer alternative.

"[Homeowners] want to cash in and think holding cash would be safer," said Fanny Chiu, chief senior sales manager at Hong Kong Property (Services), adding that Tuesday’s violence had "definitely" prompted sellers to slash prices.

"Potential buyers also said they wanted to see what would happen on October 1 to decide whether to buy or not," said Chiu, noting that the current sentiment is acutely bearish.

As for evidence of a decline in prices over the past week, SCMP cites two examples.

On Wednesday, the owner of a 378 sq ft flat at La Cite Noble in Tseung Kwan O lowered the asking price by 7.1 per cent, from HK$7 million (US$892,700) to HK$6.5 million.

A day earlier, a 919 sq ft flat at Lake Silver in protest-hit Ma On Shan sold for HK$13 million, after the price was slashed by HK$3.3 million, or 20.2 per cent.

And that's a particularly serious problem for HSBC, which has underwritten many of the mortgages on Hong Kong homes. That's right: The protests could seriously destabilize the 6th-largest bank by assets in the world.

Our friends at the Strategic Macro Blog recently took a look at the cockroaches in HSBC's basement and laid out how vulnerable the bank truly is to the economic shock brought on by the protests

So conventional wisdom is that post-Basel III the banks hold a lot of capital against loans and are run conservatively. And in a normalised market this is very true I think.

However when you are calculating LTVs and RWAs and PDs against bubble valuation levels, are they still appropriate? If you calculated it against replacement costs, the LTVs would go through the roof, and so would RWAs and the banks would be left with an CET tier 1 equity deficit to be covered by a rights issue. Any losses and higher RWAs on impaired loans would further cost equity.

So Hong Kong real estate which yields 1-3% rental yields in many cases, vs a Prime lending rate which is 5.15% is an enormous, negatively carrying bubble, propped up by speculation and Chinese capital flows.

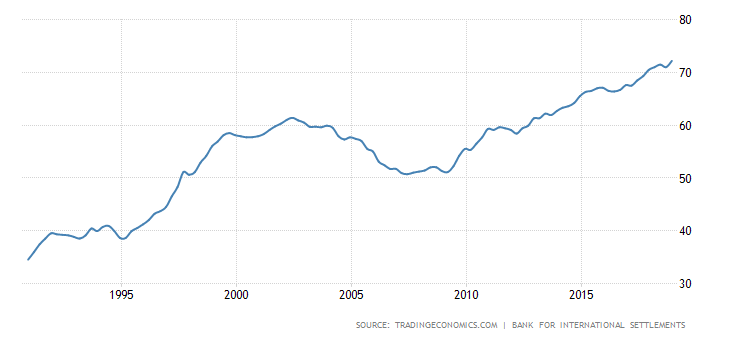

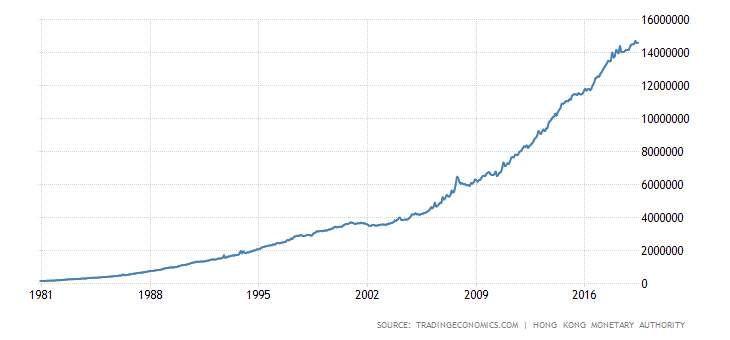

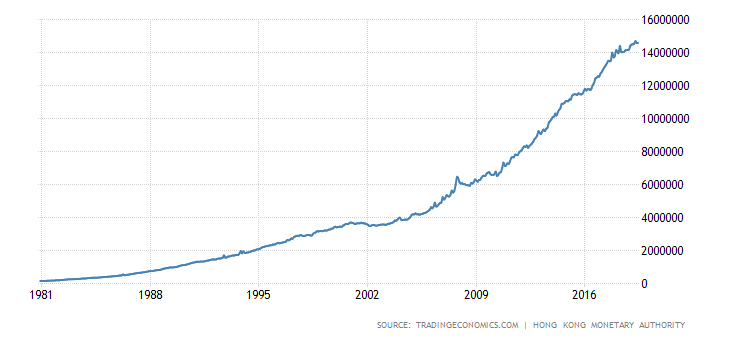

HSBC is the 800lb gorilla in a banking system where M3 is >5x GDP.

M3 and Household debt to GDP:

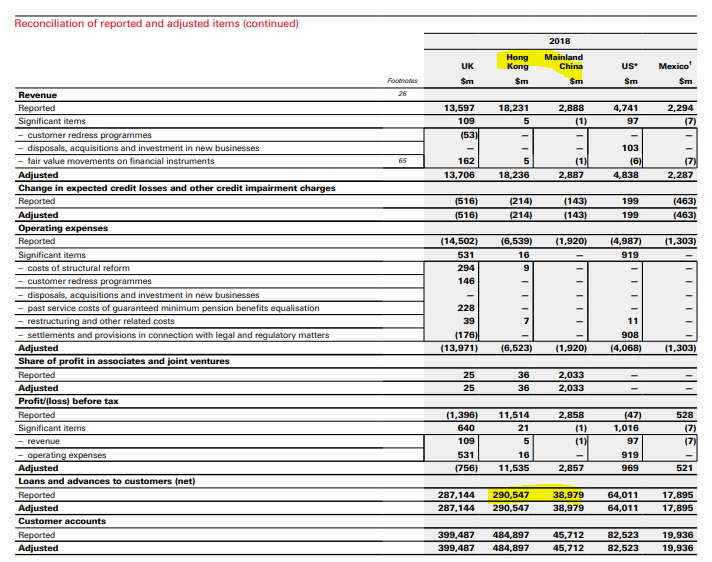

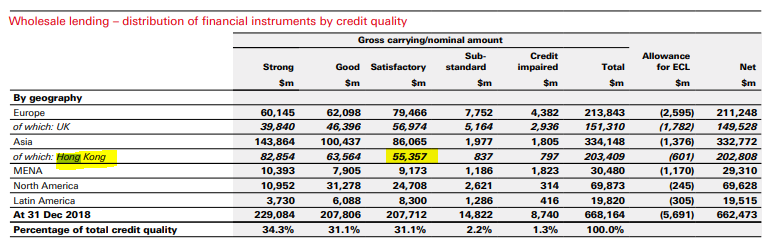

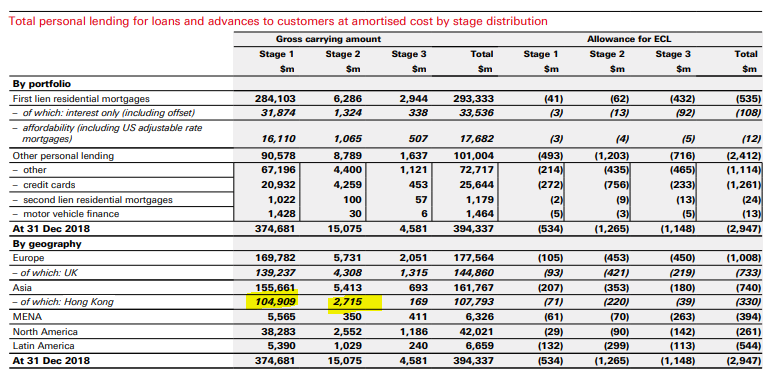

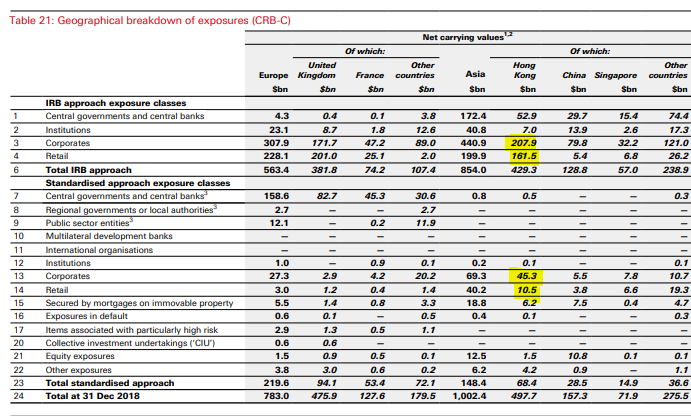

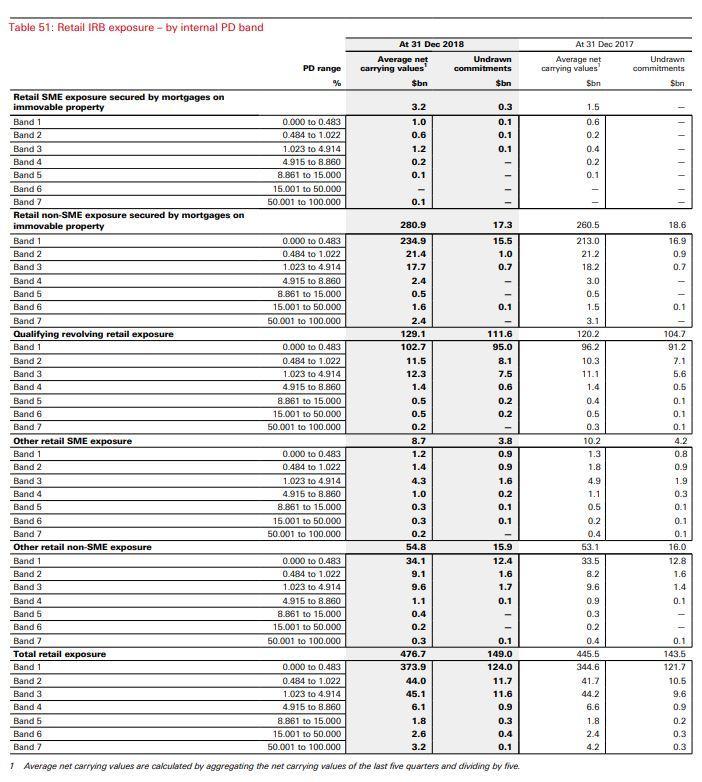

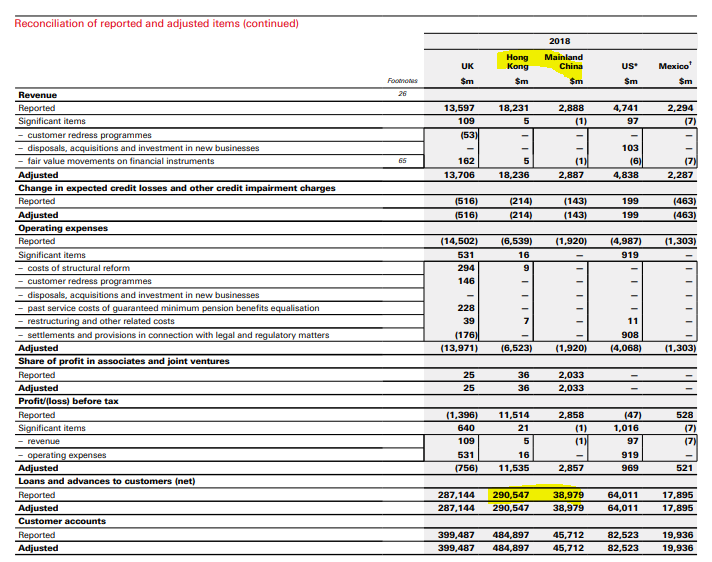

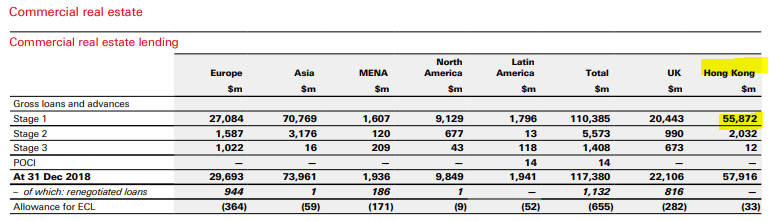

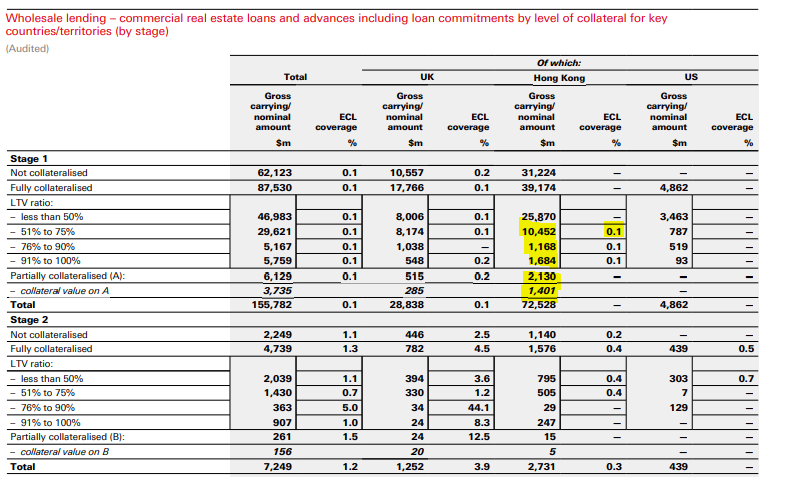

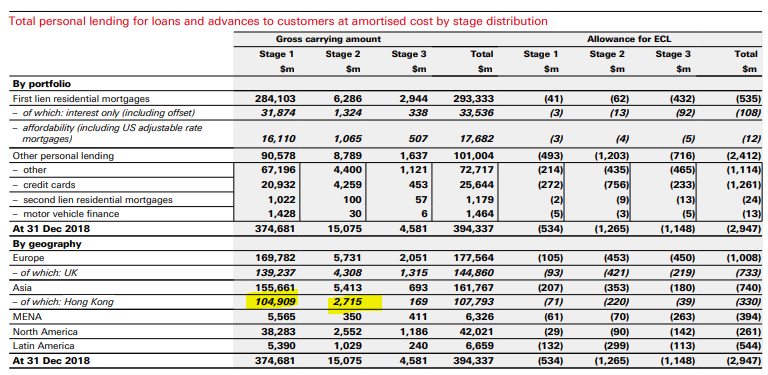

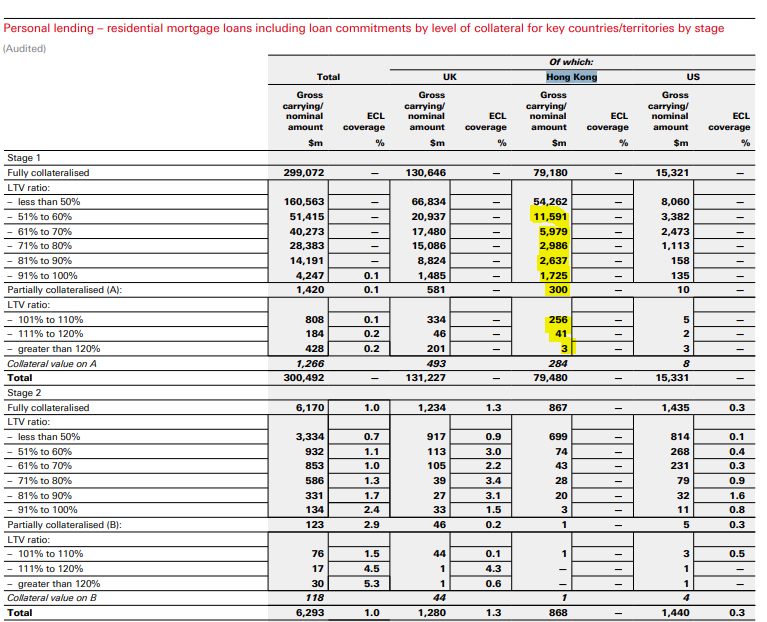

Here are some excerpts from HSBC's financials and Pillar 3 statements for Dec 18.

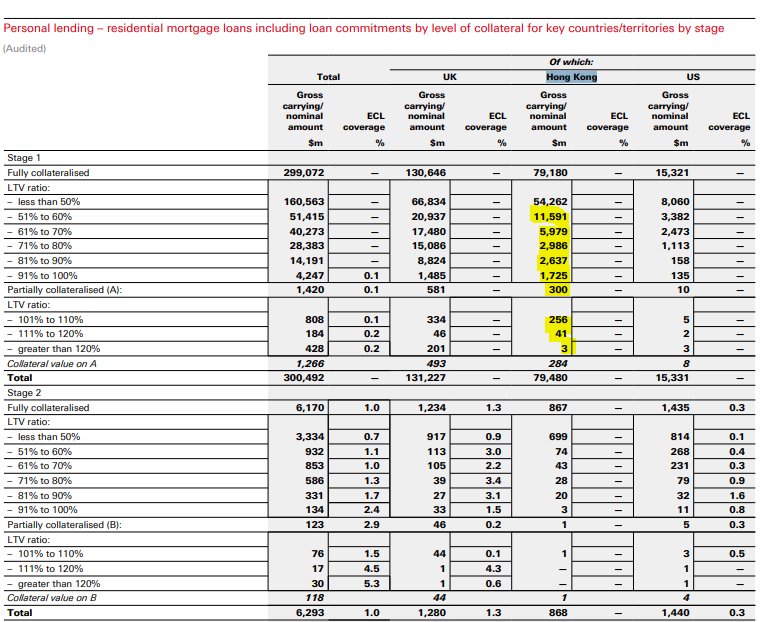

HSBCs 2018 AFS. $300bn plus exposure to HK and China.

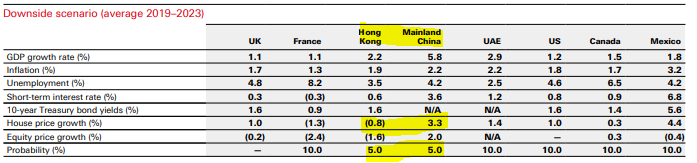

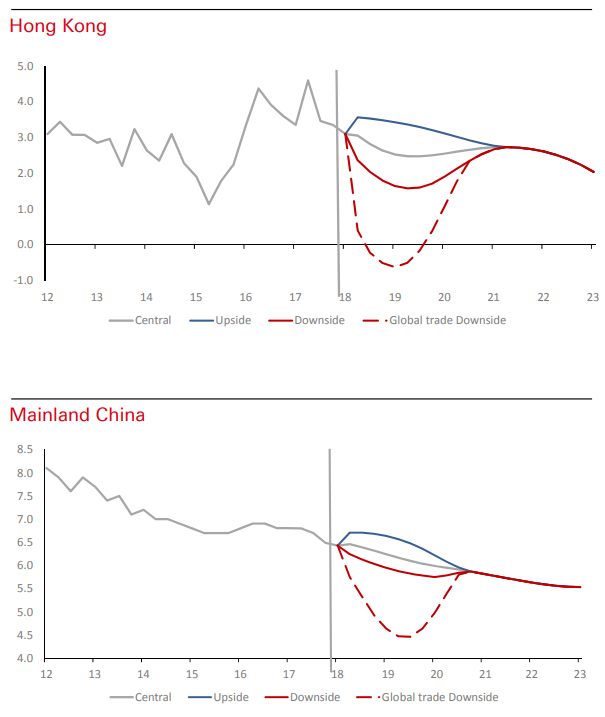

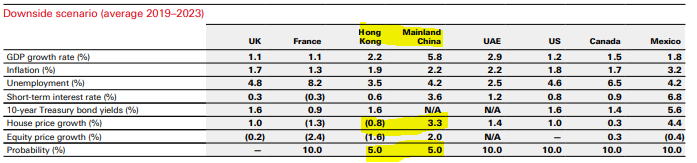

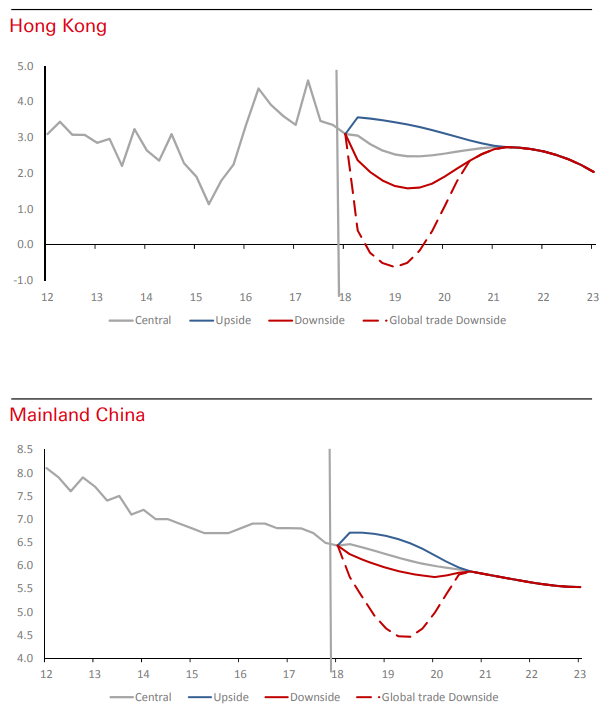

Downside risk scenario involves small house price drops and ongoing economic growth.

Trade exacerbated downside drives a greater slowdown in 2019 only with recovery in H2-20.

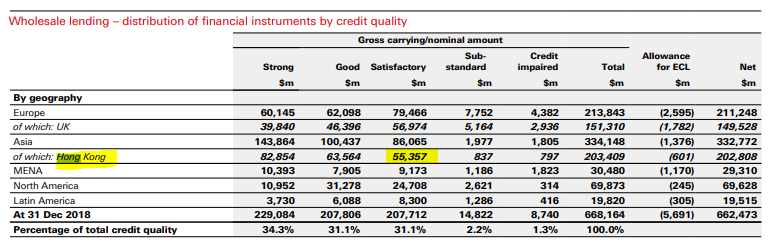

$55bn of Category 3 loans to wholesale borrowers. Category 3 typically has a 100% RWA under Basel III.

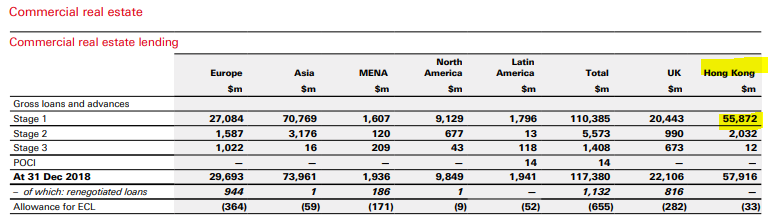

$58bn of CRE, $2bn impaired

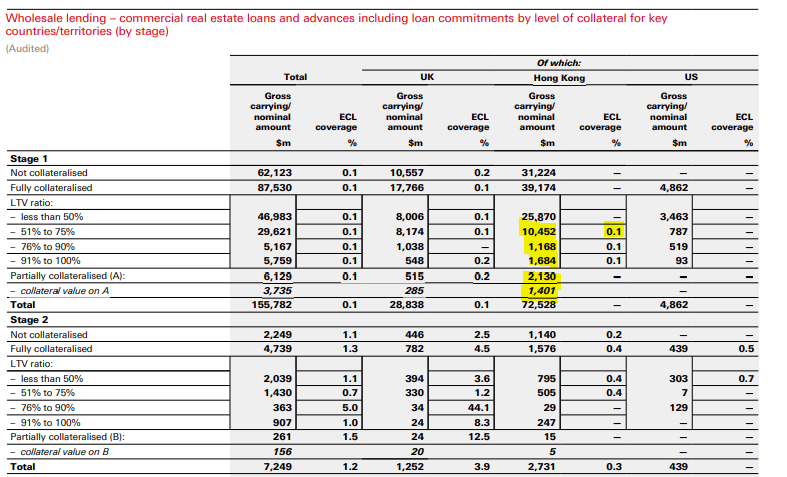

About $15bn in higher LTV wholesale loans:

$108bn in personal loans, of which about $3bn are impaired

About $25bn in loans above 51% LTV

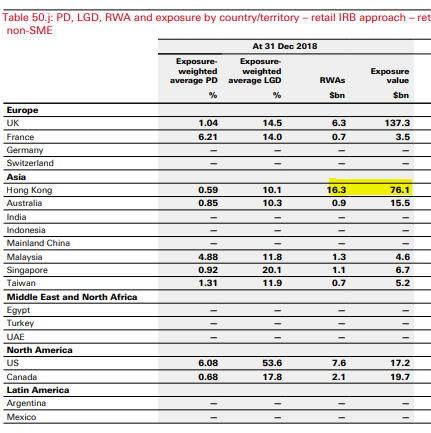

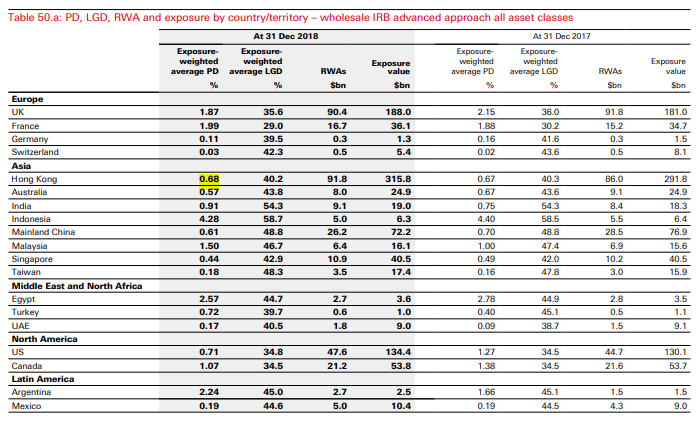

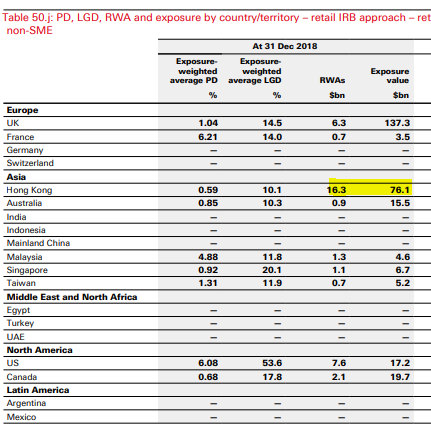

However most of their book has RWA charges determined by their Internal Ratings Based approach:

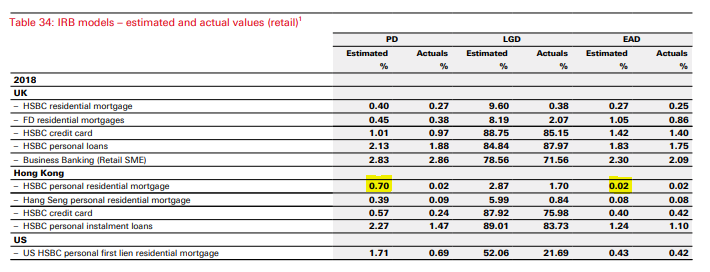

Using their IRB approach retail mortgages have only a 0.7% probability of default and a few percent of loss given default. They calculate a 20% RWA charge against this.

Wholesale loan PDs are also under 70bps and seem to be applying a 30% RWA charge.

Only by IRB derived models and applying low PDs and low LDG rates have they been able to book these loans at 20 or 30% RWA levels and as such 'Category 1 loans'. But Category 3, 4 or 5 loans carry 100% or 150% RWA charges. So any large falls in property prices and rise in PDs will absorb a lot of CET1.

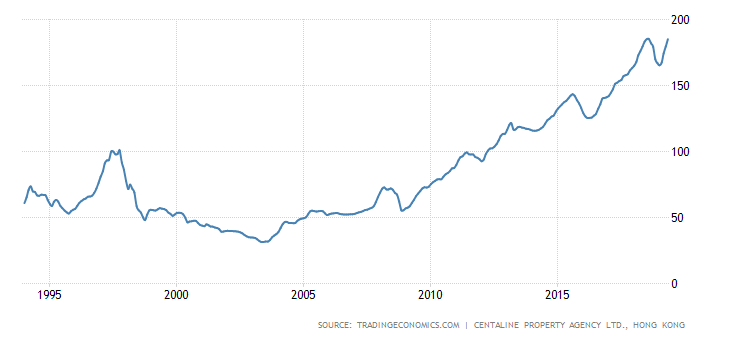

As a reminder after the 1997 bubble imploded the Honk Kong residential index dropped from 172 to 59 between 1997 and June 03, a 66% drop in nominal terms and more in real.

And remember the prime lending rate is 5.15% and property yields 1-3%. Well they have 3 year interest deferred ARM mortgages to resolve for that.... I wonder if any of HSBC's wholesale loans book is against such loans?

* * *

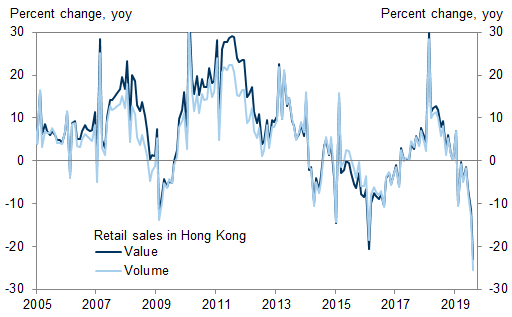

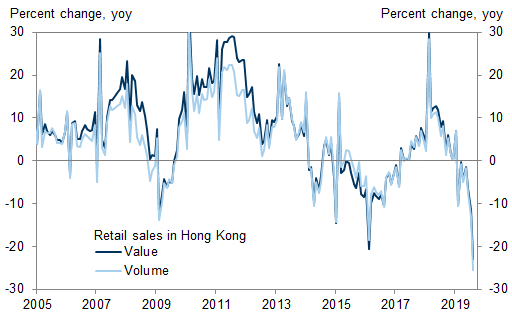

This isn't the only example of the protests' negative impact on Hong Kong's economy. Retail sales contacted by 23% YoY in August, the largest decline on record. Compared with the prior month, retail sales dropped by just about 12.5% in August, following a 5.2% contraction in July.

The fall in spending spread as far as Europe, where luxury goods makers saw their shares impacted by the protests. As Hong Kong's economy deflates, it's virtually guaranteed that more Hong Kongers will support Xi Jinping when the CPC finally decides that it has had enough of the unrest.

No comments:

Post a Comment